At the end of 2021, China had 26 GW of offshore wind installed, of which 17 GW was installed in 2021, adding more capacity than the rest of the world had installed over the previous 5 years, and stealing UK’s end 2020 crown of 10 GW of installed capacity.

Germany had 8 GW of offshore wind as of the end of 2022. It has offshore wind targets as follows:-

- 2030 – 30 GW

- 2035 – 40 GW

- 2045 – 70 GW

The German grid picks up the costs of transmission of power from an offshore wind farm to the onshore grid connection.

Germany has one way CfD (contract for differences) auctions for offshore wind. The cheapest bids win the auctions. “One way” means that the the generator has the wholesale market price of power made up to the contracted strike price for the project if the wholesale price is lower. But if the wholesale price is higher than the strike price the generator does not have to pay back the difference.

However this has resulted in many recent zero price CfD auction bids for German offshore wind, which means the generator just takes the wholesale market price. This has resulted in lotteries to determine the winners, with other criteria also being taken into account. This isn’t really satisfactory. The process is being amended but the current proposal is contentious.

Existing German offshore wind capacity factors are listed on this link.

Japan has huge potential for offshore wind power, with around 550 GW possible – mainly with floating offshore wind.

At the end of 2022, the UK had 13.7 GW of offshore wind installed, and a 2030 target of 50 GW offshore wind. Taking into account likely capacity factors, this implies that the 2030 UK grid will likely be 70% powered by offshore wind, with some also available for export.

RenewableUK has analysed the UK and global offshore wind projects. As of February 2023, the UK pipeline of offshore wind projects is 100 GW, broken down as follows:-

UK offshore wind farms capacity factors are listed on this link.

The UK exclusive economic ocean zone has huge offshore wind potential – enough to provide the energy required by the UK in 2050 two to three times over.

UK’s exclusive economic ocean zone is 773,676 sq km and includes Rockall and the Isle of Man. With a conservative estimate of the average offshore wind power density of 300 kW per sq km, this equates to 232 GW average available, which is 2,033 TWh per year. The UK CCC (Committee for Climate Change) estimates the total 2050 UK total energy requirement to be up to 680 TWh per year [p45].

By the end of 2022 the USA had almost no offshore wind installed – 42 MW – but the pipeline of projects is large and extending over time.

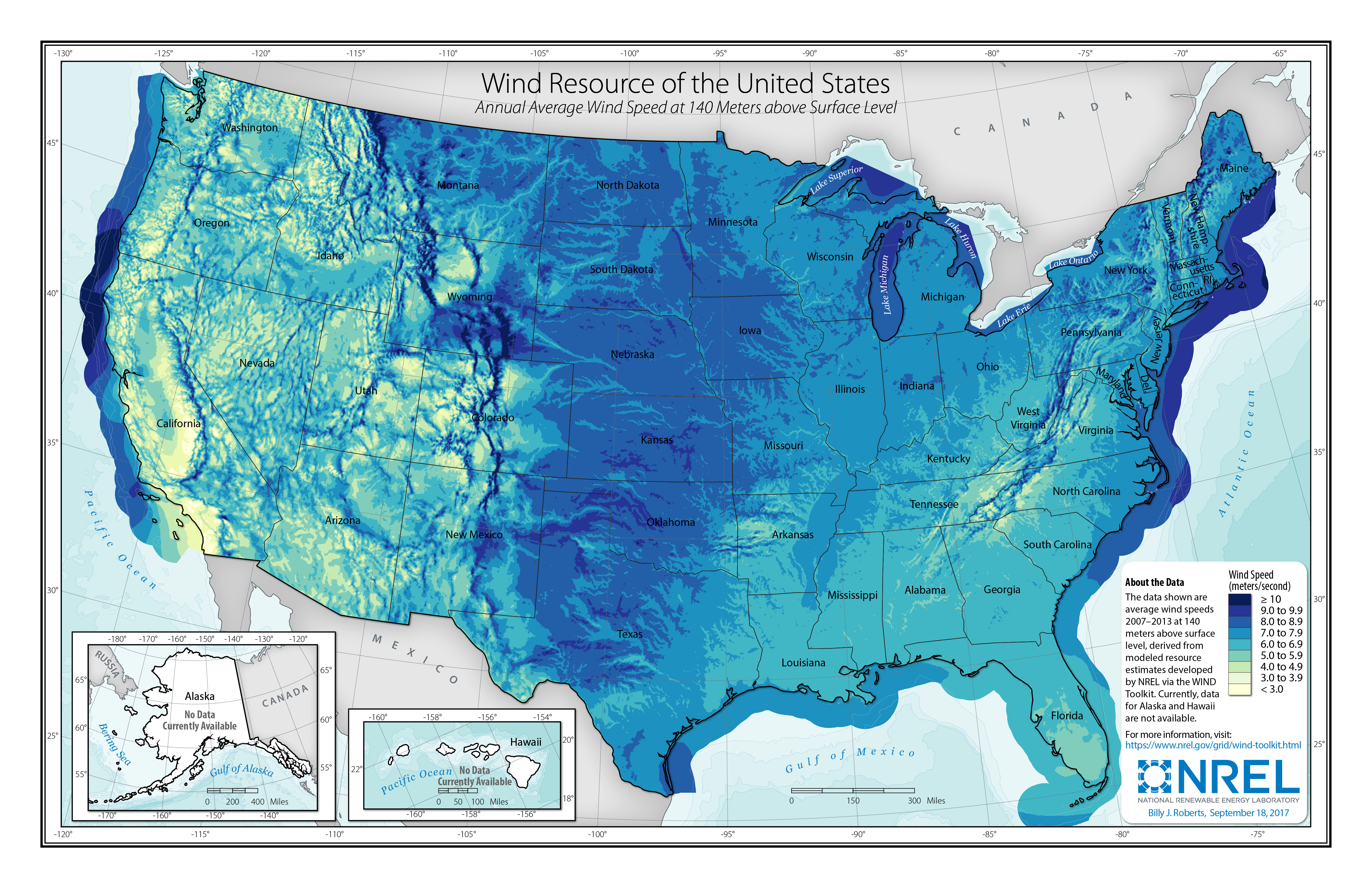

However, as can be seen from the NREL US wind map below, the USA has plenty of offshore wind resources on both coasts.

The US Biden administration has a target of 30 GW of offshore wind by 2030, plus 15 GW of floating offshore wind by 2035. Most of the US coastline is suitable for bottom fixed offshore wind, but northern California, Oregon and Maine have steeply sloping sea bottoms for which floating turbines will be required.

Most US coastal states have shown strong interest in offshore wind.

The US BOEM (Bureau of Ocean Energy Management) has issued a list of offshore wind leases and a lease area atlas. California has just concluded an auction of floating offshore wind and there are a number of lease auctions coming up.

The US IRA (inflation reduction act) provides for a 6-30% tax break for offshore wind farms. The higher amounts require the project to conform to certain wage and apprenticeship provisions.